Sequence of returns risk

Once a portfolio is funding life, the order of returns can matter as much as the returns themselves.

Sequence of returns risk is the risk that the same investment returns produce different outcomes depending on the order they arrive in, once money is being withdrawn from the portfolio.

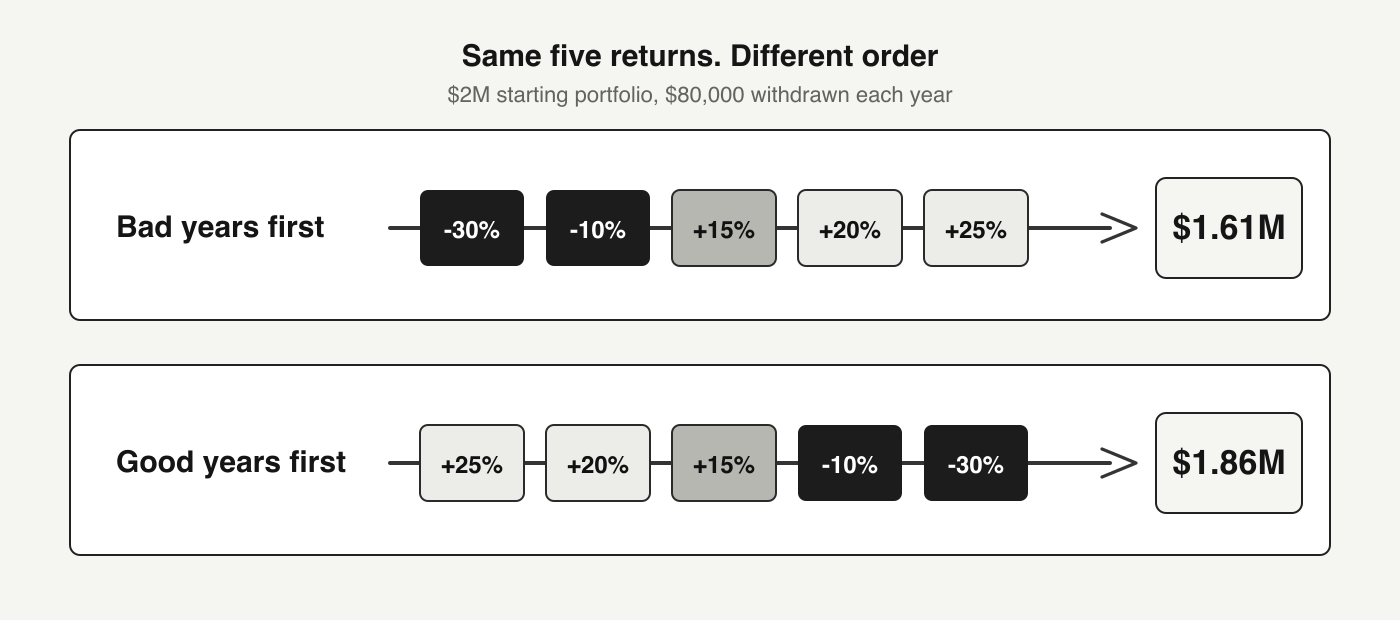

Start with $2 million and withdraw a fixed $80,000 at the end of each year: 4% of the starting portfolio. One five-year path is -30%, -10%, +15%, +20%, +25%. Another path uses the same five returns in reverse order.

Without withdrawals, both paths end in the same place: about $2.2 million.

Once withdrawals begin, the order matters. The bad-first path ends around $1.61 million after five years. The good-first path ends around $1.86 million.

The five-year gap is roughly $250,000.

But the deeper problem is that every later year compounds from the smaller base.

By year 15, the gap is about $535,000.

By year 25, it is about $1.16 million.

That $1.16 million gap is more than fourteen years of $80,000 withdrawals that never had a chance to compound.

Same returns. Different order. Different life.

Why withdrawals change the math

Average return stops being enough once the portfolio has to fund life.

If no money is moving in or out, the order of annual returns does not change the final value. The same returns in a different order end at the same number.

Once withdrawals start, the order matters.

Bad early years do more than create paper losses. They shrink the base of capital while the portfolio is also funding life. Each withdrawal comes from a smaller base. The later recovery helps, but it has fewer dollars left to compound. It cannot compound on dollars that have already been spent.

The simple version: markets fall soon after the portfolio starts funding life, and the recovery has fewer dollars to work with. Selling while prices are down is how temporary losses become lasting damage.

The long-term average can look healthy while the early path breaks the plan.

Money going in vs. money coming out

Bad early returns can help when money is going in and hurt when money is coming out.

When money is going in, early losses still hurt, but new savings are invested at lower prices. The recovery is not doing all the work by itself. A bad early sequence can even help if the investor keeps buying through the drawdown.

When money is coming out, the portfolio has to repair itself without fresh capital coming in, while also paying for life. Early losses shrink the base, and withdrawals come out of that smaller base. The portfolio is trying to recover while it is still wounded. That is how a temporary drawdown can become lasting damage. Dollars sold after a drawdown are no longer there for the rebound.

Recovery time still helps. But once withdrawals begin, the portfolio has to rebuild while money is still coming out.

Why it mattered after the exit

After selling my business, I was not just choosing an asset allocation. The exit created real freedom, but not immunity from math. I was asking whether a finite portfolio could support my family for decades, starting much earlier than traditional retirement.

That turned sequence risk into one of the main design problems.

The usual answers tend to work around the problem: withdraw less, keep a stock-heavy portfolio, hold a cash cushion, add private investments, hire an adviser, or accept a more conservative version of life. Some of those choices are reasonable. But they do not necessarily solve the sequence problem.

The obvious way to reduce sequence risk is to withdraw less. A lower withdrawal rate reduces pressure on the portfolio. But it also pays for sequence risk in advance by making life smaller. A 3% life and a 6% life are not the same life.

A stock-heavy portfolio can sound like a more ambitious answer: accept volatility, trust the long-run return, and wait. But if the plan still depends mostly on equity-like risk being rewarded soon enough, smoothly enough, and in the right order, the plan still has a sequence problem.

That is why risk parity became interesting to me. It was not another plan built around equity risk carrying most of the load. Equities still matter as one of the main engines of long-term growth. The risk parity insight was that equities did not have to carry the withdrawal plan alone.

Combining return streams with different reasons for working and sizing them by risk is how the portfolio is built to create a smoother path without simply lowering the withdrawal rate.

That is the mechanical link to sequence risk: a shallower early drawdown means withdrawals come out of a less damaged portfolio, so the bad order does less permanent damage. The upside is not just less pain. If the early path is less damaging, the same capital can support more spending without depending as much on a lucky sequence.

How I use the term

When I say sequence of returns risk, I mean the withdrawal problem: losses arriving early, after money has started coming out.

It is not a prediction that bad returns are coming, and it is not just another name for volatility. The problem also does not disappear just because stocks tend to win over long periods.

Long-run returns still matter. But the term forces a different test: can the portfolio survive the bad years arriving first?

Designing for a bad sequence

If the bad years arrive first, can the portfolio design make them less destructive without simply shrinking the life the exit was meant to support?

The answer starts with return streams that do not all need the same kind of market to work. A risk parity-style portfolio goes further by sizing those streams so one bad run in one stream is less able to dominate the whole withdrawal path.

In my own system, that means sizing three main return streams: equities, Treasury exposure, and trend following. Equities still provide long-term growth, but they are not the only stream carrying the withdrawal plan through a bad early sequence. Treasury exposure and trend following add return streams with different drivers, so the plan is not just waiting for equities to recover.

For a portfolio that is withdrawing, a shallower hole early often matters more than a higher peak.

What I test

The long-run average is not enough. I want to know what happens if the first decade is ugly.

That means testing the depth of early drawdowns, the length of the recovery, how much selling happens while the portfolio is down, whether one return stream dominates the withdrawal path, and whether the portfolio still works when the good years arrive late.

That is why sequence of returns risk sits underneath so much of my portfolio work. It is why risk parity became interesting to me, why I care about return streams like trend following and Treasury exposure, and why I keep testing whether the added complexity actually makes the withdrawal path more durable.

I am testing all of it against the same question: can the portfolio survive a bad order of returns while money is coming out?

What can still go wrong

Sequence of returns risk cannot be eliminated.

Even a carefully built mix of return streams can still get a bad sequence. Leverage can magnify a weak design. Different-looking investments can still depend on the same underlying risk.

The goal is not to find a perfect allocation. It is to know whether the portfolio has been built and tested for the withdrawal problem, not just average return.

The real question

Once the portfolio is supporting the life the exit was meant to buy, can it survive the bad years arriving first, or did the plan depend all along on the good years showing up at the right time?